It’s already been more than seven years since the UK confiscated Venezuela’s gold reserves.

Last week, Venezuela’s Interim President Delcy Rodríguez sent a letter to King Charles III of England kindly asking him to release the Venezuelan gold reserves that have been impounded in the Bank of England’s vaults for the past seven years. The reserves, she said, are needed to finance reconstruction efforts after last month’s devastating twin earthquakes.

“That gold belongs to our people,” Rodríguez wrote in the letter. “It is to address the consequences of the [June 24] earthquake”.

When the 31 tonnes of Venezuelan gold was confiscated, in early 2019, it was worth roughly $1.9 billion. Since then, however, the price of the yellow metal has more than doubled. Based on today’s prices, those 31 tonnes of gold are now worth approximately $4.06 billion.

That’s a lot of money for a country that has been hit by its biggest natural disaster in decades, shortly after suffering the most severe peace-time economic contraction of any country in recent history, as Mark Weisbrot documents in an article for the Washington-based Center for Economic and Policy Research (CEPR):

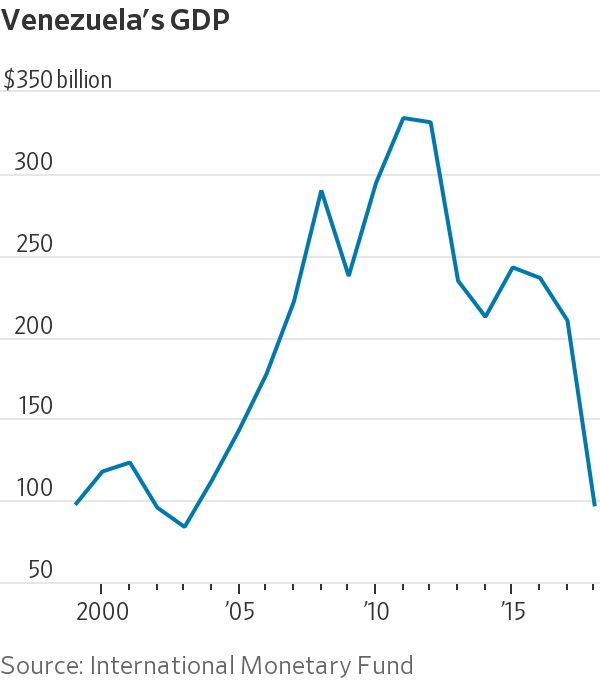

Data from the International Monetary Fund show a 74% decline in its GDP during that time [2012-20]. This is a loss of income about three times larger than what people here in the United States experienced during the Great Depression of the 1930s.

This was not a natural disaster like the earthquake, but a man-made one. IMF data show that 88% of this loss took place following U.S. economic sanctions that began in 2015. The destruction accelerated with the Trump sanctions, starting in 2017, that cut the country off from most international finance and then from the vast majority of its foreign exchange earnings. These shocks would have pushed almost any country into a severe crisis, and that’s exactly what happened, demonstrating to the world how sanctions really could destroy an economy.

Here’s a graphic illustration, courtesy of the Wall Street Journal, of the damage inflicted by two main events: the collapse of oil and commodity prices in 2014, and the US’ suffocating sanctions in the years that followed:

Economic conditions have, unsurprisingly, deteriorated since the US’ January 3 military attack on Venezuela and abduction of President Nicolás Maduro, who is now being kept in solitary confinement in a New York prison more than 23 hours a day.

Francisco Rodríguez, also of CEPR, estimates that Venezuela’s economy grew 2.5% year over year in the first quarter, its weakest performance in years, even as the country’s oil exports jumped 25%. The reason is obvious: the US is keeping a large piece of the action rather than sending it to Caracas.

Meanwhile, the death toll from the earthquakes has reached 3,800 and is likely to continue to grow in the coming weeks. According to UN estimates, the economic impact of the quakes could reach $37 billion, or 32% of Venezuela’s already anaemic gross domestic product.

An increasingly unpopular Delcy Rodríguez is desperate to get her hands on Venezuela’s sovereign funds to speed up reconstruction, revive economic activity and restore education services in the affected areas. But that is unlikely given most of the sanctions are still in place and the person who has the final say on such matters is US Secretary of State Marco Rubio.

From the New York Times’s article, “How Marco Rubio Is Running Venezuela from Afar“:

In the six months since U.S. forces blew open Maduro’s bedroom door and snatched him in the dead of night, Rubio has become the de facto viceroy of Venezuela, holding sway over a sovereign nation in a way that no U.S. official has since Paul Bremer arrived in Baghdad in 2003 to run U.S.-occupied Iraq.

Rubio now effectively controls Venezuela’s finances, the distribution of its natural resources and its government, according to interviews with more than a dozen officials and people close to both governments in Washington and Caracas, who provided details about his involvement in steering the country’s policies. Many spoke on the condition of anonymity to describe private interactions and internal discussions.

While he has not visited Venezuela in person since the U.S. took over, Rubio is deeply involved in the country’s day-to-day operations, keeping in close contact with Delcy Rodríguez, who was Maduro’s vice president and now leads her country on an acting basis, with the imprimatur of the United States.

But not just of the United States. Israeli officials and soldiers are also back in Venezuela for the first time since Hugo Chavez broke off diplomatic ties and expelled the Israeli ambassador and his staff over the 2008-09 Gaza War.

As we have been warning in recent months, the US’ hostile takeover of Latin America — whether through military force, like in Venezuela, or rigged elections, like in Honduras and Colombia — has helped open the door for growing Israeli influence in the region.

Meanwhile, it’s not just Venezuelan oil that is flowing to the US; so too are other critical minerals, including, ironically, gold. By late March, less than three months after the US military intervention, the Trump administration had brought back $100 million of gold from Venezuela for U.S. refiners, according to Interior Secretary Doug Burgum.

In the clip below Burgum is barely able to contain his excitement as he tells FOX News that Venezuela has “$500 billion of resources of gold” under its soil as well as other critical minerals “we need for defence and consumer goods”.

Now, to the confiscated gold. Roughly 31 tons of Venezuelan gold was impounded in January, 2019 after the UK government decided to recognise Juan Guaidó as Venezuela’s president. Even before then, the Bank of England had refused to allow the Maduro government to withdraw its gold, citing concerns about the legitimacy of Maduro’s election victory in late 2018.

Once Guaidó proclaimed himself president of Venezuela from a city square in downtown Caracas, with Washington’s backing, London began facilitating Guaido’s legal battle to seize the country’s gold held at the BoE. In the end, Guaidó was unable to pull off the heist due to legal appeals launched by Venezuela’s real government in Caracas, though he did burn through hundreds of millions of dollars of Venezuelan funds seized by the US and put at his disposal.

In the meantime, Venezuela’s gold still sits frozen in the Bank of England’s vaults (or does it?) — more than three years after Venezuela’s leading opposition parties voted to oust Guaidó as “interim president” and dissolve his parallel government.

From UK Declassified’s article “Why Is Venezuela’s Gold Still Frozen in the Bank of England?“, published in January 2023:

[T]he UK government insisted at every turn that it recognised Guaidó – and not Nicolás Maduro – as Venezuelan president. In turn, Guaidó’s lawyers argued that he was authorised to represent and control the assets of the Central Bank of Venezuela held in London.

Throughout this time, Guaidó paid his UK legal costs by drawing on millions of dollars of his country’s assets originally seized by the US government. In other words, Guaidó tried to seize Venezuelan state assets with looted Venezuelan state assets.

Meanwhile, it seems certain that the Foreign Office also used a significant amount of public funds to sustain its backing of Guaidó.

Now that Guaidó has been ousted, the legal argument for transferring the gold to the Venezuelan opposition has effectively disintegrated. Despite this, the gold remains frozen in the Bank of England, with no clear resolution in sight.

Whatever happens next, this case sets a precedent which could have far-reaching consequences: the UK’s coup weapons now include asset stripping a foreign state, and transferring those assets to political actors engaged in regime change.

This will surely serve as a warning to any state which plans to store its gold in the Bank of England.

So it has proven. As we reported in January, German economists and politicians have been intensifying their calls, which began over a decade ago, for the full repatriation of Germany’s gold reserves, of which roughly half is stored abroad, mainly in the US and the UK. Keep in mind that Berlin had to wait five long years to repatriate just 300 tons of its gold from the US Federal Reserve. Plus, it never got back any of the gold bars originally deposited.

Which begs the question: is Venezuela’s gold still in the Bank of England’s vaults? Has it been sold off, leased out, as happens with a lot of central bank gold, or “rehypothecated”?[1] Given the long history of manipulation in London’s gold market, the massive disconnect between the paper markets for gold and the physical markets, the apparent lack of external audits, just as with the FED, and the recent signs of gold shortages in London, nothing can be ruled out…

Click here to read the full article on Naked Capitalism