Open-end funds have grown significantly over the past two decades and now manage around $41 trillion in assets globally. And the risks they pose to the global economy are growing, says the IMF.

A new report from the International Monetary Fund underscores the dangers that so-called open-end (or open-ended) funds could pose to the global financial system, including potentially tightening financial conditions and exacerbating market volatility during times of heightened stress. Open-end mutual funds are investment vehicles that use pooled assets and are always open to investment. In other words, investors can take out part or all of their money any day of the week.

A $41 Trillion Market

These funds have grown significantly over the past two decades. Many mutual funds, exchange-traded funds and hedge funds are open-ended. According to the IMF, open-end funds now manage around $41 trillion in assets globally — equivalent to roughly one-fifth of the non-bank financial sector’s holdings. As Investopedia notes, they “are more common than their counterpart, closed-end funds, and are the bulwark of the investment options in company-sponsored retirement plans, such as a 401(k).”

The region of the world with the highest concentration of open-end mutual funds is Europe, which is already in a world of (largely self-inflicted) economic pain. According to Statista, the old continent was home to 59,000 such funds at the end of 2021, compared to 33,000 in the Americas, 38,000 in the Asia Pacific region and 1,710 in Africa.

As the IMF report notes, open-end funds play a large role in the financial system, “offering investment opportunities to investors and provide financing to companies and governments.” But they can become a serious problem when the assets they hold are not nearly as liquid as the daily redemptions they offer to their investors.

When large numbers of investors decide to redeem their funds en masse, such as during a financial crisis, those funds have no choice but to sell assets in the portfolio to raise enough money to meet those redemptions. As long as the assets are highly liquid, such as large cap stocks or government bonds, this is normally manageable.

But when the assets in question are high-yield bonds, loans, commercial real estate or large positions of thinly traded small-cap stocks that can take days, weeks or even months to sell, there is a mismatch in liquidity between what the fund offers to its investors (daily liquidity) and what the fund holds (largely illiquid assets). This is a major downside of these types of open-end funds, notes the report.

Such a liquidity mismatch can be a big problem for fund managers during periods of outflows because the price paid to investors may not fully reflect all trading costs associated with the assets they sold. Instead, the remaining investors bear those costs, creating an incentive for redeeming shares before others do, which may lead to outflow pressures if market sentiment dims.

First-Mover Advantage

The inevitable result is a mad rush to the doors. Sophisticated investors are usually the first to make the move. When enough investors try to use the so-called “first-mover advantage” by pulling their money out before everyone else does, the open-end mutual fund faces a “run on the fund” and is forced to sell large volumes of illiquid assets to meet redemptions. But the only way to sell them quickly enough is to sell them at ever lower prices. The longer investors stay in the fund, the more they lose.

When this happens on a large enough scale, setting off a feedback loop of accelerating redemptions and falling asset prices, it can end up posing a risk to the financial system itself, warns the IMF paper.

Pressures from these investor runs could force funds to sell assets quickly, which would further depress valuations. That in turn would amplify the impact of the initial shock and potentially undermine the stability of the financial system.

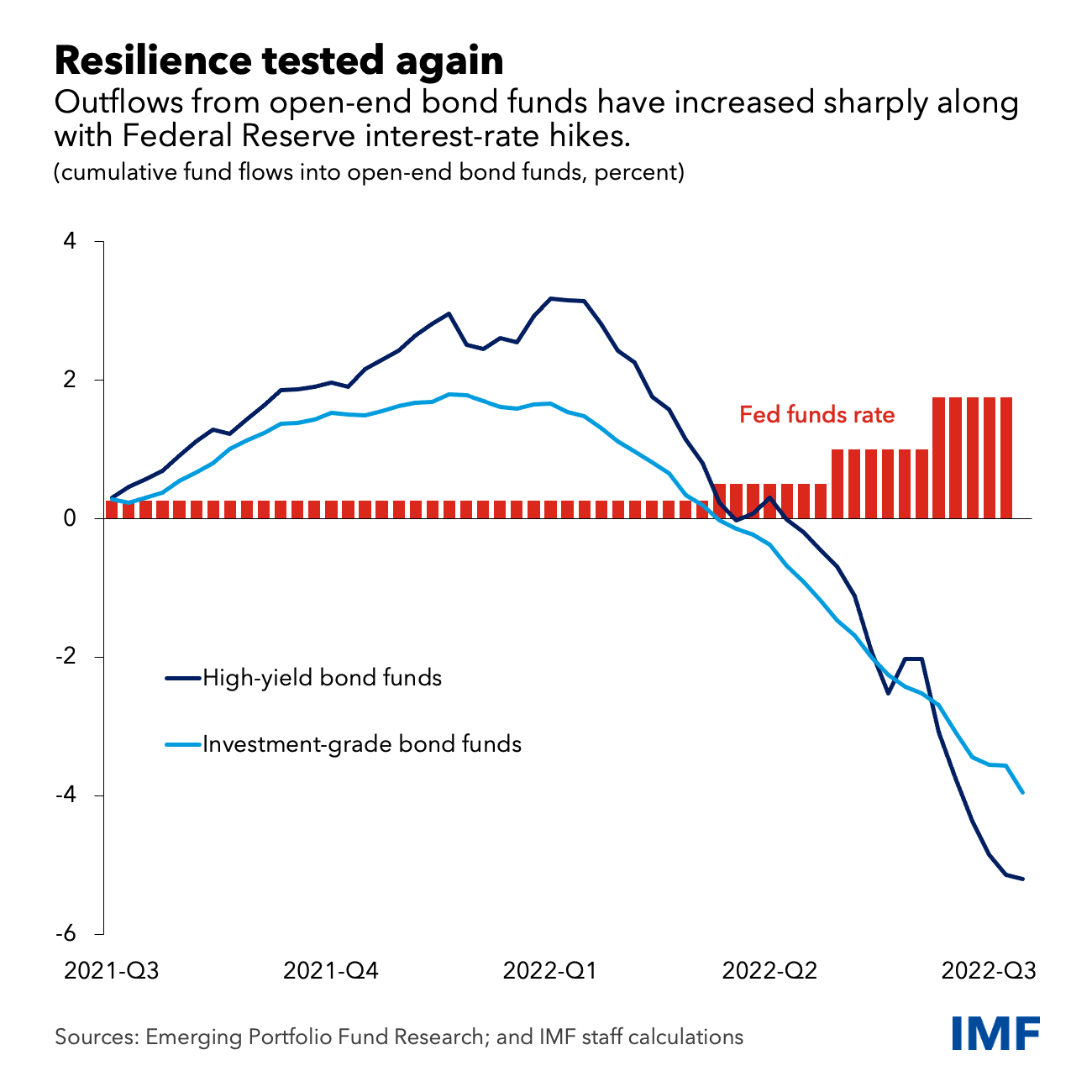

Right now, the pressures are rising as central bank tightening has triggered a surge of outflows from open-end bond funds.

Been Here Before

This is not a new problem, or one that has just suddenly become apparent, such as, say, UK and US pensions funds’ predilection for exotic derivatives. During the global financial crisis many open-end funds were upended by the liquidity mismatch deathtrap. They included a family of bond market funds marketed by the Charles Schwab Corporation as conservative alternatives to money market funds during the lead-up to the Global Financial Crisis. As my former WOLF STREET colleague Wolf Richter noted in a 2019 retrospective, they turned out to be anything but conservative:

The top 10 holdings, which is what investors could see listed, was the usual mix of Treasury securities and investment-grade corporate bonds, and some highly rated corporate paper. Beneath the skin, 45% of the funds’ holdings were mortgage backed securities (MBS), including many backed by subprime mortgages. Most of them were highly rated as well.

But smart investors in Schwab’s conservative-sounding open-end bond mutual fund kept their eyes on the markets. And when the tide turned in the housing market, they started paying attention, and then they saw that people were defaulting on mortgages, as home prices were dropping.

This was the first warning sign. These astute investors sold their shares of the fund back to Schwab and got their money out, after having earned the juicy yields for years. They had the “first-mover advantage” because what came after them turned into a nightmare for slow-poke investors.

As the waves of redemptions intensified and accelerated, Schwab sold off more and more of its liquid assets, until just about all that was left on its balance sheets were MBS. By that time the subprime crisis was in full swing, the mortgage meltdown was all over the media and the value of those MBS was in free fall:

From its $14 billion in assets in 2005, the fund dropped to $13 billion in May 2007, to $6.5 billion in January 2008, to $2.5 billion in March 2008, to $500 million in July 2008, to about $210 million in October 2009, by which time the fund had been shuttered.

As Wolf notes, investors in the funds who didn’t panic first, or at least early enough, ended up losing the lion’s share of their money:

Unlike the prices of stocks or bonds that investors hold outright, bond mutual funds that experience a run cannot recover because the fund is forced to sell the assets, and they’re gone, and when prices of those assets recover, someone else owns them and takes the gain. A run on the fund is a one-way event that is a permanent loss to fund holders.

In the aftermath, lawyers got rich on the ensuing legislation and hedge funds, distressed debt funds and others that bought the distressed MBS for cents on the dollar from the Schwab fund made a killing by selling them at face value to the Fed.

A Particularly British Problem

Today, broad sell-offs are once again rippling across the financial system as central banks hike rates and reverse their asset buying programs in a desperate (and probably vain) bid to tame inflation, which is largely being driven by supply chain factors. The recent mayhem in the UK’s gilt markets has triggered a rapid sell-down of higher risk assets by heavily levered pension funds as they scramble for cash to meet collateral demands…

Read the full article on Naked Capitalism