“An upside surprise to inflation is among the greatest risks”; we’d need “to tighten policy even more rapidly or on a more significant scale, or possibly both, in a way that would take the legs out of the recovery.”

“The situation we need to avoid like the plague is one where inflation expectations adjust before we do, or where we wait for proof positive that effects on inflation are not transitory before acting,” said Bank of England chief economist Andy Haldane during the Treasury Select Committee this week. “Because in both of those cases that would be doing too little too late.”

It’s not everyday you hear a central banker of an advanced economy voicing concerns about runaway consumer price inflation. Most of the time, central bankers are doing everything they can to play down such fears. The current price increases, they say, are “transitory” or “temporary,” and as such nothing to worry about. Haldane disagrees:

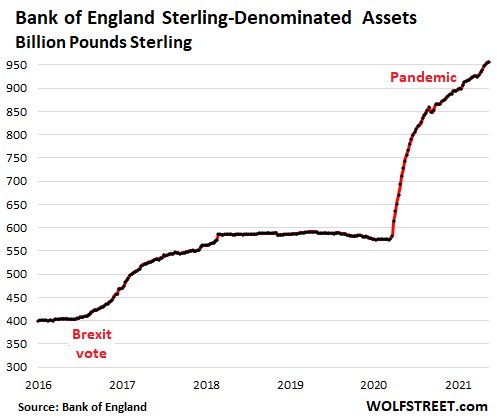

With interest rates at zero, “give or take”, and with the government and Bank of England injecting “unprecedented-in-peacetime fiscal and monetary stimulus” into the economy, Haldane believes that tapering the BoE’s bond purchases is not enough; it’s time to “turn off the tap,” he says. “This is serious money, edging up toward £1 trillion of QE.”

“It’s clear if you speak to businesses across the UK right now that among the top three issues is this pipeline of very significant cost rises. It’s hard to find very much, whether it’s goods or assets, that aren’t going up right now, with the honorable exception of Bitcoin.”

Haldane’s comments are also noteworthy given that consumer price inflation in the UK is not yet nearly as high as it is in the US and other economies. It more than doubled in April, mainly on the back of higher energy prices and clothing costs, but it still clocked in at just 1.5% in April, up from 0.7% in March — a lost less than the 4.2 % increase in the Consumer Price Index in the US.

Haldane won’t be chief economist and executive director of monetary analysis and statistics at the Bank of England for much longer. He is scheduled to leave the Bank in June, having taken up an offer to become chief executive of the Royal Society for Arts in September.

But before he leaves, Haldane is making a few waves. In the last meeting of the Monetary Policy Committee (MPC) Haldane was the only member to vote to lower the UK’s quantitative easing program by £50 billion, to £845 billion, citing inflation concerns. And that, it seems, has touched a few nerves. David Blanchflower, a former member of the MPC, said that while dissenting voices on the panel were important, Haldane was dissenting on the wrong side:

“He should not have been saying there’s going to be lots of inflation. There isn’t. Most of what he said was based on wild guesses and wishful thinking. It’s not what you’d expect from the chief economist, but what you might expect from a commentator on a news program.”

Unlike the Fed, the BoE doesn’t have an open-ended QE program, but has set a target of bringing its holdings of UK government bonds to £875 billion and its holdings of corporate bonds to £20 billion, for a combined target of £895 billion. And like the Bank of Canada, it has already begun to gradually taper its bond purchases, from £4.4 billion a week to £3.4 billion a week.

This stimulus, together with a host of other factors — including low inventories, supply chain shocks, rising shipping costs, surging demand for certain commodities and consumer goods in developed economies — is fueling inflation. Unlike most of his colleagues at the BoE, Haldane believes that inflation, now that it’s arrived, is unlikely to be transitory…

Continue reading the article on Wolf Street