They haven’t gotten over Financial Crisis 1 and the Euro Debt Crisis. Now there’s a new crisis. Deutsche Bank’s CEO going on TV to soothe nerves didn’t help matters.

The biggest European banks have started to report their earnings against a bleak backdrop of locked down economies, plunging economic activity, surging business closures and rising loan defaults. Each earnings call laid bare the scale, scope and complexity of the problems and challenges facing a European banking sector that never really recovered from their last two crises — the Global Financial Crisis followed by the Euro Debt Crisis.

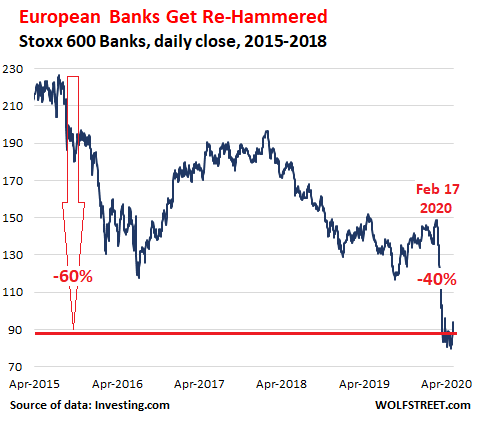

The Stoxx 600 Banks index, which covers major European banks, fell 4.5% on Thursday. Today, continental European stock markets were closed (May Day), but the London Stock Exchange was open, and the index ticked down another 1% (to 88.8). The Stoxx 600 Banks index has already collapsed by 40% since Feb 17, when the Coronavirus began spreading through northern Italy. After the initial 40%-plus plunge in late February and early March, the index has remained in the same dismally low range:

On April 21, the Stoxx 600 Banks Index had closed at 79.8, down 83% since its peak in May 2007, and the lowest since 1987. The following day, the ECB announced it was going to accept junk bonds as collateral when banks borrow from it. Yesterday, the ECB was excepted to go even further and announce that it would actually buy junk-rated bonds, as the Federal Reserve announced a few weeks ago. But the ECB didn’t announce it, and the Fed hasn’t bought any junk bonds yet either.

Unlike the Fed, whose 12 regional Federal Reserve Banks are owned by the banks in their districts, and to whom bank stocks are therefore hugely important, the ECB couldn’t care less about bank stocks, as long as the banks themselves don’t collapse. The ECB’s primary focus is on keeping the Eurozone together, a task that is growing more difficult by the day.

Now that we are in the grip of yet another full-blown financial crisis, triggered not by the banks this time, but by a pandemic and the response to it, central banks are throwing just about everything they can at the crisis, which is moving far faster and wider than the last one.

Continue reading the article on Wolf Street