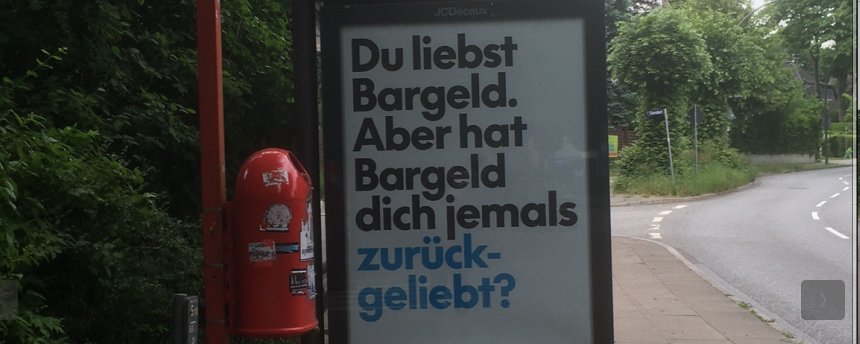

“You love cash. But has cash loved you back?”

This is the rather peculiar message splashed across a billboard at Duisburg Central Station, in Western Germany. Billboards seen in Frankfurt declare that “Cash is no longer King” — which isn’t (yet) true in Germany — or bear the slogan: “Pay later? Cash can’t do that.” What makes these cryptic anti-cash messages that have been cropping up across German cities and along roadsides in recent days particularly strange is that it is not clear who is behind them. They are bereft of company name or logo.

Given as much, there is, by necessity, a speculative edge to this article. There is no way of knowing with total certainty who is paying for this covert information campaign against cash in one of Europe’s most stridently pro-cash countries.

That said, there are clues that point in a particular direction. According to the German financial journalist Norbert Häring, the most likely culprit is the US fintech giant PayPal. The circumstantial evidence is certainly striking. In early May, PayPal published a press release (in German) announcing plans to launch a mobile phone wallet for paying at checkouts in German brick-and-mortar stores (machine translated):

In the coming weeks, PayPal will launch its first contactless mobile wallet – with Germany as its first global market… In the future, consumers will be able to pay securely and conveniently via smartphone, tapping to pay wherever contactless Mastercard payments are accepted. In addition, for the first time they will receive a complete overview of their online and offline purchases on the PayPal app.

Even the style and colour scheme of the font used in the ads roughly match those used in previous PayPal ads:

Buy Now, Pay Later

Another clue comes from the billboard slogan:

“Pay later? Cash can’t do that.”

Unlike most rival mobile wallets, the PayPal app won’t be limited to instant transactions. Shoppers will have the option to split their payments into 3, 6, 12 or even 24 monthly instalments. As the billboard brags, cash can’t do that!

Another curious coincidence: in its press release, PayPal does not mention even once its two main rivals in the mobile wallet space, Google and Apple Pay. Instead, its pitch is focused almost entirely on the limitations of cash and its declining use in Germany:

“The more the technology develops, the harder it is to ignore the advantages of digital payment,” says Jörg Kablitz, Managing Director, PayPal Germany, Austria and Switzerland. “Cash continues to play a role, but we know that many consumers and businesses are ready for innovative alternatives. We are convinced that PayPal has more to offer than cash. Our app makes paying by smartphone in the store easy and secure. Customers have the flexibility to decide how and when they pay – and can even save money in the process.”

It is not unusual for a fintech firm or payment processing company to aim their sharpest invective at cash, as opposed to their direct corporate rivals. For the US payment duopoly of Mastercard and Visa, which generate fees by facilitating money transfers between bank accounts, cash has long been their main rival. In 2010, the then-CEO of Mastercard (and current president of the World Bank), Ajay Banga, openly declared war on cash:

“In today’s terms, only 3% of retail spend in India or in China are through electronic payments. The rest is cash. I have declared war on cash; I believe MasterCard will grow by growing against cash. If you keep looking at 3%, everybody’s a rival; if you look at the remaining 97%, everyone’s a partner.

Mastercard and Visa have played arguably the biggest role in demonising cash over the years. But it seems that PayPal is joining the bandwagon now that it, too, is offering a digital payments app for physical retail checkouts, putting it in direct competition with physical notes and coins. And it has decided to launch its app in Germany, one of the most important bastions of physical currency in Europe, just as the war on cash there is escalating rapidly.

Cash’s Last Stand?

Though cash use in Germany has declined in recent years, physical notes and coins are still the main payment method, much to the chagrin of the financial and political establishment. After all, Germany is Europe’s biggest economy and together with neighbouring Austria and some countries in Southern Europe, particularly Spain, it is holding back Europe’s transition into a fully digital economy.

In 2023, 51% of all transactions in Germany were still being made with cash, with debit cards in a distant second place at 27%, according to the Deutsche Bundesbank’s annual payments survey. In many advanced economies, including the UK, Australia, Norway, Sweden, Finland and Denmark, around 10-20% of transactions are made with cash. In a survey by the European Central Bank, 69% of Germans said that cash was “important” or “very important” to them.

However, a loose alliance of banks and payment card companies is determined to change this. A few months ago, some of Germany’s biggest banks announced that they were joining forces with large credit card companies in an attempt to force cash out of the market through cartel pricing and unfair competition. From Häring’s article, Banks Form Discount Cartel to Displace Cash – Bundesbank Provides Cover (in German, machine translated):

The new initiative “Germany pays digitally”… is not an “initiative”, but a cartel. It consists of Commerzbank (Commerz Globalpay), Deutsche Bank, Volks- and Raiffeisenbanken (VR Pay), Mastercard, Visa, Flatpay, Unzer and SumUp. Further cartel members are expressly welcome to join. The aim is to displace their main competitor, cash, and the cash service providers through price dumping… cash incurs costs that are often lower for small merchants than the costs of digital payments, but not zero.

Here’s how it will work: the cartel will be offering small merchants and retailers with up to €50,000 in annual turnover free installation of a payment terminal and free use of it for all transactions for up to one year. No fees, no commissions. Those will obviously kick in during the second year. As Häring notes, the cartel members are willing to accept temporary losses in order to incentivise small businesses to accept digital payments instead of cash.

Meanwhile, the availability of cash and the ability to use it to pay for basic services is being squeezed from all sides. Earlier this week, it was announced that bank customers will soon no longer be able to get cash back from Shell petrol stations. According to a report by Frankfurter Rundschau, as of June 30 1,300 Shell petrol stations will no longer provide the cash back service to customers of Deutsche Bank, Postbank, Commerzbank and Hypovereinsbank.

For many people, the cash-back service was a simple, round-the-clock solution at a time of increasingly scarce banking services. Bank customers were able to withdraw up to €1,000 with each purchase. The move is likely to hit rural communities particularly hard since many of them no longer have bank branches or ATMs, in part due to the recent rise in ATM bombings. In the absence of banking services, many of these communities had grown to depend on Shell’s cash back services, notes the Frankfurter Rundschau report:

The vanishing options for withdrawing cash… are becoming a problem, especially in rural areas, due to the lack of bank-Shell cooperation. There, the gas stations were an effective means of withdrawing money.

Banks such as Deutsche Bank and Post Bank say they are offering alternative options in its place. Post Bank, for example, has been offering its customers a “Cash Code”, which is essentially a bar code that allows them to deposit or withdraw cash sums of up to €1,000 at over 12,000 retailers nationwide. But there’s a catch: in order to use the code, you must have a smartphone, an internet connection and the corresponding bank app.

Deutsche Bank is looking to adopt a similar approach in the coming months. As the Frankfurter Rundschau article notes, many older people still do not have a smartphone. Many of those that do will struggle to use the bank app, meaning that accessing cash is becoming more and more difficult for the one key demographic that most uses it.

Yet the same banks that are driving this trend will claim that the public’s gradual shift away from cash is purely the result of technological trends and shifting customer preferences. As the pro-cash activist Brett Scott notes, the financial sector’s escalating assaults on cash have created a feedback loop that constantly reinforces the impression that people are turning their back on cash when, in actual fact, banks are making it harder for them to access it while both bricks-and-mortar businesses and governments are making it harder to use it.

This is all happening as the European Central Bank prepares to launch a “digital euro”, which will be competing directly (and probably unfairly) with cash. As we warned in March, there are myriad reasons why Euro Area citizens should be terrified of the stealthily approaching central bank digital currency, including the threat it will pose to financial privacy and anonymity as well as the programmable features it is likely to offer, which have the potential to revolutionise the very nature of money.

Increasing Competition in Europe’s Digital Payments Market

It is against this backdrop that the online payment giant Paypal has chosen Germany as the first national market to launch its contactless payment app. As Euro Weekly reports, to make this happen, PayPal is introducing its own virtual debit card, fully integrated into the app:

This means users can pay in-store without needing a physical card or even opening a third-party digital wallet. Everything happens within PayPal’s app. It’s clean, simple, and in line with how consumers already use the platform…

What’s more, PayPal is also introducing a cashback system, rewarding users who choose to pay via their smartphones in-store. While full details on rates and conditions are still to come, it’s clear that partner retailers will play a key role, and the incentive may be enough to get users to leave their other digital wallets behind.

This launch also reflects a growing shift in the digital payments landscape, particularly in Europe. Thanks to the Digital Markets Act (DMA), which forces tech giants like Apple to open up their NFC systems to third-party apps, PayPal can now access iPhone hardware that was previously locked to Apple Pay. In short: Apple no longer has exclusive control, and competitors like PayPal are finally able to innovate on equal footing.

While this is a welcome step, it is still telling that in its press release PayPal aims its competitive focus squarely on cash and not on its other rivals in the mobile payments space. Whether PayPal is behind the dissemination of anti-cash ads that have sprouted in recent days, it is impossible to know, for the simple reason that nobody has taken responsibility for those ads. But if it is, it is taking on a form of payment that endured centuries of use and continues to enjoy strong public support in Germany, as well as many other European countries.

If German cash advocates wanted to respond in kind by launching their own counter-information campaign, they would have plenty of material at their disposal (albeit probably a far smaller marketing budget). Here are a few examples…

Continue reading on Naked Capitalism